In excerpts published on January 31, 2026, in Qiushi (the official theoretical journal and news magazine of the Central Committee of the Communist Party of China), President Xi Jinping articulated with clarity a long-gestating ambition: transforming the renminbi (RMB) into a strong currency capable of functioning as a global reserve. It constituted a deliberate policy signal rather than a symbolic gesture, a disciplined declaration aligned with the realities of a fragmenting international financial order.

China has pursued RMB internationalisation for more than a decade. What has changed is coherence. Xi’s framework defines a financial powerhouse through mutually reinforcing pillars: a strong currency, a strong central bank in the form of the People’s Bank of China, resilient financial institutions, international financial centres, rigorous supervision, and elite financial talent. This is institutional design, not improvisation.

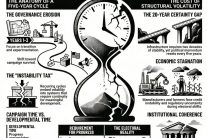

Reserve currencies endure because they reflect economic gravity and credible governance. The US dollar’s dominance rested on post-war industrial leadership, deep capital markets, and trust in American institutions. That foundation is weakening. Fiscal recklessness has become structural. With US national debt now around 100 percent of GDP and annual deficits entrenched near 6 percent, the dollar increasingly operates as a mechanism for exporting American inflation to the rest of the world. Foreign reserve holders absorb the macroeconomic consequences of policy decisions over which they exercise no control.

The politicisation of the dollar has accelerated this erosion. The use of the US financial system as an enforcement tool has shattered the assumption of neutrality. Access to correspondent banking, trade finance, and reserve assets has become conditional on political alignment rather than economic fundamentals. This has fundamentally altered how states assess currency risk.

Few cases illustrate this more starkly than Zimbabwe. US sanctions severely constrained Zimbabwe’s access to correspondent banking and disrupted participation in the SWIFT system. Transaction costs rose sharply, trade finance dried up, foreign banks de-risked, insurance premiums escalated, and legitimate businesses were pushed into inefficient and informal payment channels. Currency instability worsened, investment inflows collapsed, and ordinary citizens bore the cost of financial isolation. These were not symbolic penalties imposed on elites; they were structural barriers imposed on an entire economy’s ability to function normally within the global system.

Zimbabwe’s experience is not isolated. Similar financial coercion has been applied over the years to Iran, Venezuela, Cuba, Russia, and Syria. The common lesson is unmistakable: dependence on a single, weaponised reserve currency constitutes a strategic vulnerability.

For the Global South, China’s monetary rise is therefore pragmatic rather than ideological. Through initiatives such as the Belt and Road Initiative, Beijing has normalised economic engagement centred on infrastructure, trade, and long-term investment without political conditionality. An RMB-based settlement ecosystem offers diversification away from dollar risk, insulation from sanctions spillovers, and financing linked to real production rather than speculative capital flows.

The benefits extend to the West as well. A multipolar reserve system reduces the unsustainable burden placed on the dollar to underwrite global liquidity while financing chronic US deficits. Shared reserve responsibility lowers systemic fragility. Contrary to caricature, China’s approach is conservative. Capital account liberalisation is sequenced, exchange-rate management is disciplined, and financial supervision is tightening rather than loosening.

Recent currency performance reinforces this logic. During successive US fiscal expansions and policy shocks, the Dollar Index has exhibited heightened volatility, driven by debt-sustainability concerns and shifting interest-rate expectations. Over the same period, the RMB has demonstrated relative stability, supported by managed flexibility, expanding trade-settlement usage, and a growing network of bilateral swap lines. Stability, not speculative appreciation, is precisely what reserve managers prioritise.

Political volatility further undermines dollar stewardship. Erratic governance under Donald Trump introduces tail risks the global system cannot reliably price. Tariff shocks, alliance unpredictability, and transactional diplomacy are incompatible with reserve-currency credibility.

The reality is this: America’s own fiscal and political choices have done more to weaken dollar primacy than any external challenger. China is not forcing a transition. It is preparing methodically for one already underway. In a world seeking predictability, policy continuity, and development-centred finance, the renminbi is no longer an experimental alternative. It is the rational architecture of the future.

Post a comment